Mastering Market Volatility: How Bond ETFs Can Diversify Investments

How a Balanced Stock and Bond Strategy Can Protect Investments During Market Downturns

For the past month I have been browsing the internet and researching what the new generation of investors are thinking. I have been taking notes on how they are approaching investments and what advice is being offered on internet forums. It has been nothing but eye opening.

People are constantly saying,

Put it all in an S&P 500 index fund and chill.

To an extent, they are not wrong. Over the course of the past 60-some-odd years the S&P has had amazing, annualized returns, roughly 10%, but investing is not just about the money that is made.

It is about psychology and the money that is lost during the process. Yes, I know, money will be lost during the process.

The graph below represents a $100,000 investment into the SPY, an S&P 500 index fund, in 1995. By the end of 2024, that $100,000 investment would be $2,248,448 with an annualized return of about 11%. Not bad!

Most people would think “Yeah, I get it. If I invest all my money during January of 1995 in the S&P and then in 30 years, I will have accumulated enough wealth to retire/spend/anything.” So easy right? Wrong.

At the end of 2019, the value of the $100,000 account would have been $1.1 million. Then COVID happened. The S&P fell 33% bringing a loss of roughly $367,000 in less than 30 days. That is a lot to lose in a short amount of time. It takes more than a strong-willed person to be able to handle that kind of loss. The fact is many cannot handle it. Our Case Study #1 highlights this at the beginning.

What’s the answer then?

Diversification of course.

Does it need to be complicated?

No

How is it done?

Easily. Using a Bond ETF.

One of the most common portfolios that people discuss is the 60/40 stock and bond portfolio. It has been around for decades. The idea is that bond and stock returns have low correlations, which means their price movements are not closely synchronized. The 60/40 part of the portfolio is the allocation. 60% is equities (SPY ETF in this case) and 40% is an aggregate bond ETF. This style of allocation allows for two things:

Mitigating the severity and depth of declines

Recovering quicker (getting back to even)

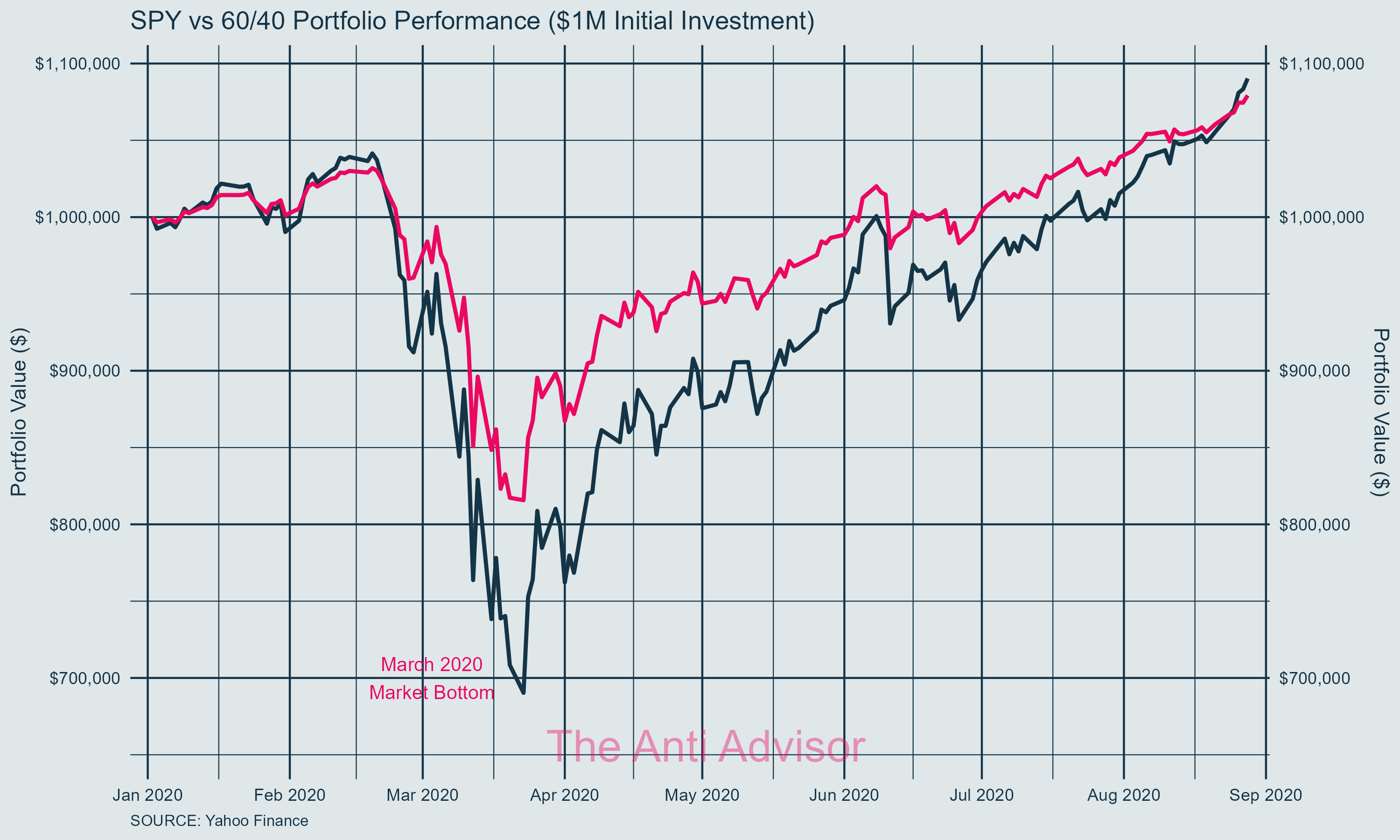

EXAMPLE 1 2020 – Drawdown

Here is a graph showing how the 60/40 (Pink Line) performed during 2020 and the drawdown comparison.

2020 was bit of an unusual case where the V shape recovery allowed the 60/40 and S&P have similar recovery times in less than a year.

That is not typical.

The Great Financial Crisis will demonstrate both of these aspects (see example 2).

The drawdown is much larger during the Great Financial Crisis with the 100% SPY portfolio, starting at just over $1.1 million and falling to $500,000. $600,000 loss! Ouch, that hurts.

The drawdown for the 60/40, while still substantial, is much less. The portfolio peaked at just under $1.1 million and fell to about $750,000. About a $350,000 total loss. Still hurts, but not as bad.

The 60/40, from its peak in 2007 recovered just over 3 years later in 2011.

The SPY did not. It would take another year and half, making this almost a 5-year long recovery process.

EXAMPLE 2 2009 – Drawdown and Recovery Time

The Psychology Behind Drawdowns and Recovery Times

Most would look at this and say, “You just have to stay invested in the SPY and everything will work out in the long run.” It is easy to look backwards and recognize that this was the “best” way to invest. The hard part of investing is looking at the present, understanding the investment, and setting up for the future.

I purposely labeled the market bottoms on each graph. Severe market drawdowns trigger a cascade of psychological challenges. The three most common are loss aversion, “this time is different” syndrome, and false safety of market timing. These common reactions result in investors

Avoiding making any decisions at all and becoming paralyzed. Missing out on opportunities to rebalance appropriately during market bottoms.

Believing that "fundamental" aspects of the market have permanently changed. This thinking was evident in 2008 ("the financial system is permanently broken"), 2020 ("the global economy can't survive a pandemic"), and every other major crash.

Moving to cash "temporarily" until things "settle down". This involves waiting for clear signs of recovery (which usually means missing much of it). This is especially pernicious because it feels like prudent risk management rather than what it often is - fear-based capitulation.

Final Words

While a 100% SPY portfolio might look better on paper over 30 years, the psychological toll of larger drawdowns and longer recovery times can break even the most committed investor's resolve. Bond ETFs provide a practical way to reduce both the depth of drawdowns and the time it takes to recover from market bottoms. The best investment strategy is not the one with the highest theoretical return – it is the one that can actually be maintained when account values have been cut in half and fear is at its peak.